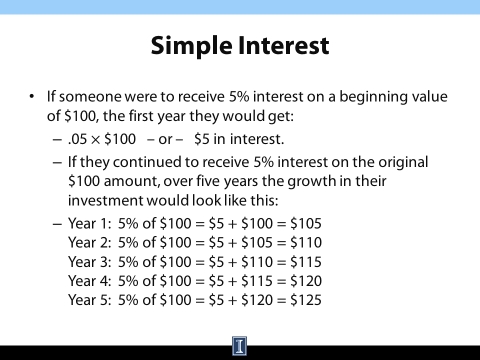

Simple interest is, well, simple to calculate. Let's start with an example. If someone were to receive 5% interest on a beginning value of $100, the first year they would get .05 (which is 5%) times 100, or $5 in interest. If they continue to receive 5% on the original $100 amount over five years, their investment would be calculated as shown on the slide.

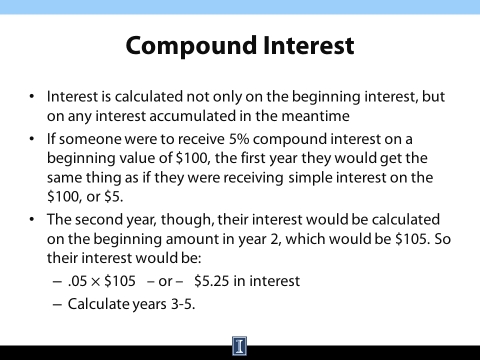

Financial institutions don't use simple interest. Instead they use compound interest. It is calculated not only on the beginning investment but also on any interest accumulated in the meantime. So if we use the same example as in the previous slide, someone to receive 5% compound interest on a beginning value of $100, the first year they would get the same thing as they would getting simple interest. You'd multiply it 5%, or .05, times $100 to get that value of $5. The second year, though, the interest would be calculated on that amount entering year 2, or $105, so the 5% still converted to .05, but that's multiplied by $105 to arrive at $5.25 in interest in year 2. Calculate years 3 through 5. The answer is provided in the note pages.

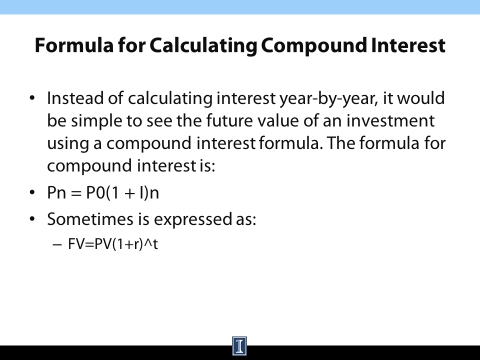

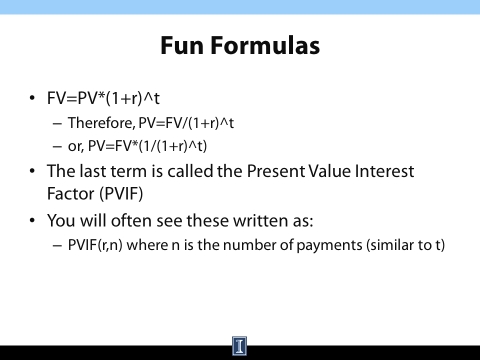

As you can see from just calculating the three years in the previous example, doing this for, say, 30 years, like the life of a mortgage, would be quite time consuming and cumbersome. Instead of doing this on a year-by-year basis, it would be simple to see the value of an investment using a formula. This is expressed commonly two different ways. The first formula is P_n=P_0 ?(1+I)?^n. P_n is the value at the end of n^ periods. P_0 is the beginning value, or the principle. I is equal to the interest, and n is equal to the number of years. Sometimes this is expressed as the future value, FV, is equal to the present value, PV, times 1+R, R being the interest rate, to the T. T is equal to time. Use the values given in the previous question of $100 and 5% for five years, to see what you would come up with using this formula.

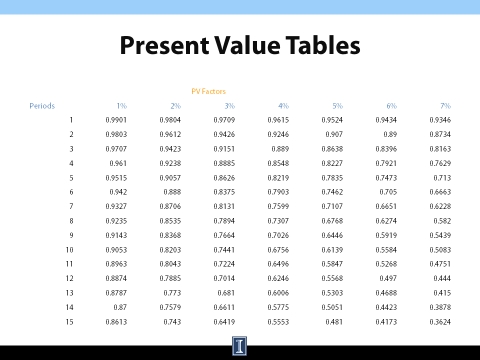

These formulas may be fun. They may not be. If you see the first line, it's just the last line from the previous slide. The future value is equal to the present value times 1+R^t. Using algebra, we can simplify this to find the present value is the future value divided by 1+R^t. So if you just keep in mind that 1+R^t is consistent, 1 is multiplied by that term while the others divided. The rest of the slide depicts the present value interest factor as well as how that's sometimes noted where you'll see the interest rate and the number of compounding periods in brackets

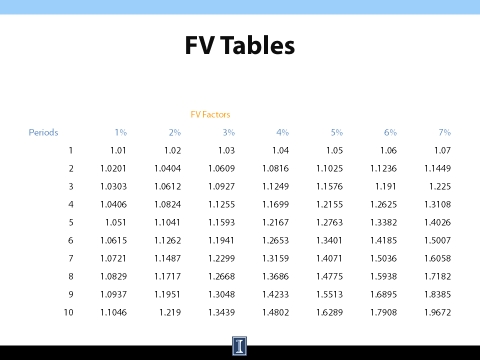

There are tables that provide these factors for use as a quick reference, so let's practice using the table using just a few straightforward questions. So if you invest $1,000 at 4% today, how much will you have at the end of eight years? To repeat, if you invest at $1,000 at 4% today, how much will you have in eight years? You use the 4% and eight years to find the interest factor and then multiply that times $1,000 to get the final value.

Question 2. If you invest $400 at 7% today, how much will you have in three years? Again, if you invest $400 at 7% today, how much will you have in three years?

Both questions and answers appear in the note pages.

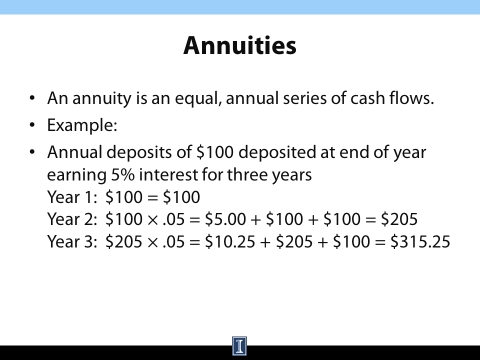

An annuity is an equal annual series of cash flows. Annuities may be equal annual deposits, equal annual withdrawals, equal annual payments or equal annual receipts. The key is equal annual cash flows. They work the way shown in the explanation in the example.

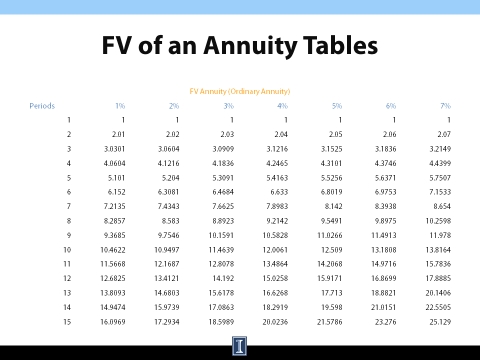

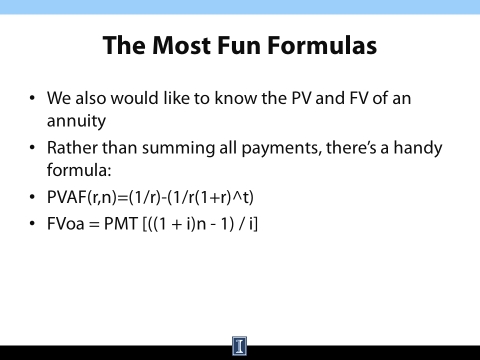

The future value of an ordinary annuity is equal to the payment PMT((1+i)^n-1)/i. You can use that formula and then check your answer with the table for the questions depicted in the notes pages.

Future value is used when you want to anticipate the value of an investment or a cost to you of borrowing in the future. Just as often we want to know what things are worth now, in today's dollars. That present value is simply the reciprocal of the compound interest of future value. Another way of thinking of it, and to see it mathematically is time zero in our future value formula.

Note that all the values are less than 1. Therefore, when multiplying a future value by these factors, the future value is discounted down to the present value. The table is used much the same way as the other time value of money tables.

We also don't want to have to calculate these one year at a time. Just like with compound interest, we would also like to know the value of an annuity using formulas. Formulas are given on the side. Keep in mind that R and i are the equivalent of one another, as are t and n. You could see these formulas appear with R or i interchangeably and n and t interchangeably. That may sound complicated, but in the end that ?(1+R)?^t always stays together. It's just a matter of finding it and seeing what works around it.

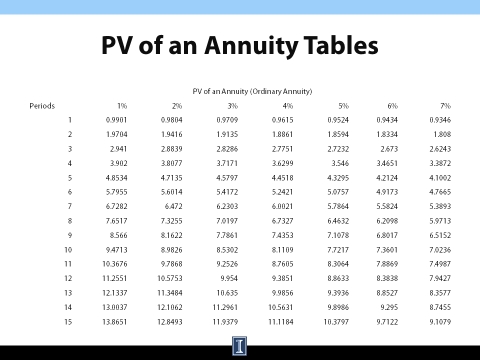

Like present value and future value compound interest, there's also tables that we can use to check present value of an annuity. Use the formulas from the previous slide to find the present value, and use the table to check your answer.

In all of the previous examples, the interest was compounded annually, but we can also compound the interest monthly or semiannually, quarterly. The examples on the next slide should help illustrate how to adjust our formula for intra-year compounding. The rules as to how to do that are provided here.

One example is given here on the slide with the answer in the note pages. Look to the note page for two additional examples with question and answer following.

AFTER SLIDE:

Using the formula it would be:

PV=CF + PVAF(r,n-1)*CF

Perpetuity is a cash flow without a fixed time horizon. To find the present value, take the annual return in dollars and divide it by the discount rate. Example follows on the next slide.

One question is given on the slide. The answer appears in the note page.

That covers all the critical elements of understanding time value of money. It seems like a lot of information going through the slides. It will get easier with practice. A number of examples are given in the worksheet. Don't hesitate to reflect back on the slides and refer back to them in order to get the best results. Some tips for showing your answer appear in the last bullet point.